Introduction: The Hidden Danger of High-Interest Personal Loans

High-interest personal loans may seem like a quick financial solution during emergencies. With instant approvals and minimal documentation, they provide fast access to cash. But what many borrowers now a days don’t realize is that high personal loan interest rates can quickly lead to a debt trap, making repayment difficult and long-term financial stability harder to achieve.

In this article, we’ll touchdown the following topics and will also discuss about practical solutions:

- How high-interest personal loans create debt traps

- Real-life examples

- Warning signs to watch for

- Practical and realistic solutions to escape debt

What Is a Debt Trap?

A debt trap occurs when a borrower must take new loans to repay existing ones due to high interest rates and unmanageable EMIs.

Instead of reducing debt, the borrower ends up:

- Paying mostly interest and the principle amount is not reducing

- Extending the loan tenure

- Damaging your credit score

- Increasing financial stress

So eventually, over a period of time, the total repayment becomes significantly higher than the original borrowed amount. Now here for the simplification of our fellow readers, I’ve summarised the entire discussion into three Major Points (A, B & C)

A — How High-Interest Personal Loans leads to a Debt Trap

1. High Interest Rates Increase Total Repayment

Personal loan interest rates can range from 18% to 36% or higher, depending on credit profile and lender.

For example:

- Loan Amount: ₹2,00,000

- Interest Rate: 24%

- Tenure: 2 Years

- Total Repayment: ~₹2,50,000+

You pay ₹50,000 extra in interest alone.

If payments are delayed, penalties and compounding would make the situation worse.

Now let’s understand the above stated fact with some Real-life examples.

2. Real-Life Example: The Emergency Loan Spiral

Rahul, a salaried employee, took a ₹2 lakh personal loan for a medical emergency at 24% interest.

Six months later:

- Unexpected expenses occurred

- EMIs became difficult to manage

- He took another loan at 30% interest

So, within a year:

- You’ve 3 ongoing loans

- 45% -50% of salary going toward EMIs

- Credit score dropped

- Collection calls increased

This is how a high-interest loan turns into a debt spiral.

3. Loan Stacking: Borrowing to Repay Borrowing

Many borrowers use:

- Credit cards to pay EMIs

- Short-term loan apps for repayment

- Buy Now Pay Later (BNPL) schemes

This creates interest-on-interest debt, making it almost impossible to reduce the principal.

4. Hidden Charges Increase Financial Burden

High-interest personal loans often include:

- Processing fees (Generally higher compared to conventional loan from Banks)

- Late payment penalties

- EMI bounce charges

- Prepayment penalties

Even missing one EMI, it significantly increases your outstanding balance.

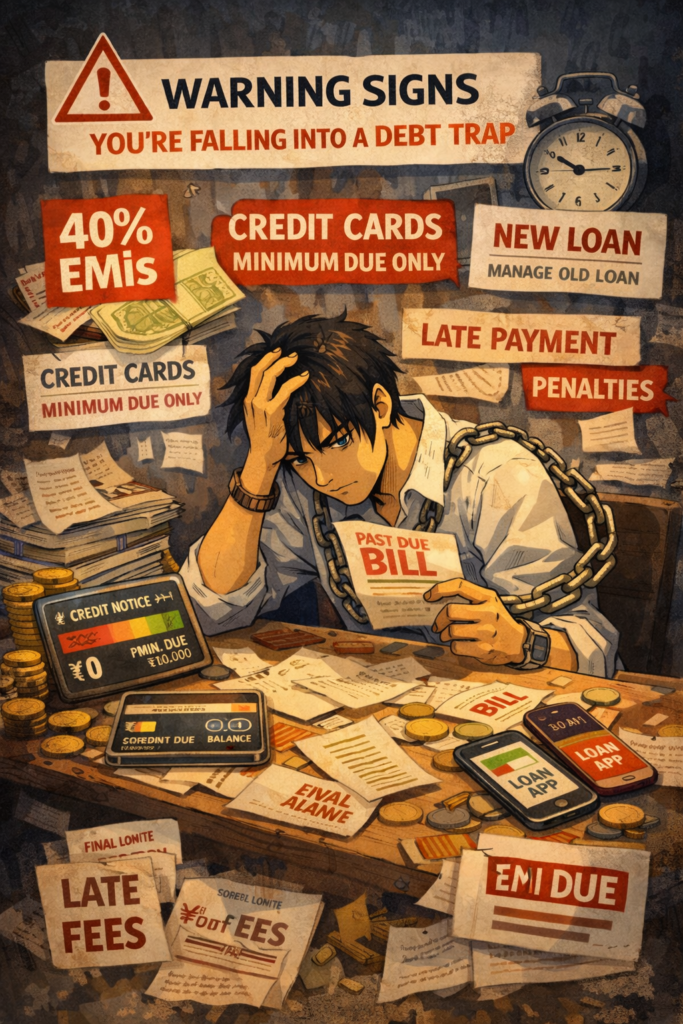

B — Warning Signs You’re Falling into a Debt Trap

Must check these red flags:

- More than 40% of income goes into EMIs

- Paying only minimum due on credit cards

- Taking new loans to manage old ones

- Frequent late payment penalties

- Constant stress about due dates

If you identify 2–3 of these signs, corrective & prompt action is urgent.

C — How to Avoid a Personal Loan Debt Trap (Practical & Feasible Solutions)

1. Follow the 30–40% EMI Rule

Your total EMIs should not exceed 30–40% of your monthly income.

Example:

If your salary is ₹60,000 → Keep EMIs below ₹24,000.

This reduces repayment pressure.

2. Build a 6-Month Emergency Fund

Instead of relying on high-interest loans:

- Save 6 months of essential expenses

- Start small (₹3,000–₹5,000 monthly)

- Keep funds in liquid savings

An emergency fund prevents borrowing during crises.

3. Compare Annual Percentage Rate (APR), Not Just EMI

Many borrowers focus only on EMI amount.

Instead of that they should focus:

- Check APR

- Calculate total repayment

- Read fine print carefully

As, paying a lower EMI amount does not always mean cheaper that the loan is cheaper.

4. Use the Debt Avalanche Method

If already in debt:

- List all loans by interest rate

- Pay highest-interest loan first

- Continue minimum payments on others

This reduces overall interest burden faster.

5. Consider Debt Consolidation (Best possible long-term solution)

If multiple loans exist:

- Opt for a lower-interest consolidation loan

- Negotiate with lenders

- Explore balance transfer options

This simplifies repayment and reduces stress.

6. Cut Lifestyle Expenses Temporarily

For 6–12 months:

- Reduce discretionary spending

- Pause subscriptions

- Avoid luxury purchases

- Consider side income

Short-term discipline prevents long-term financial damage.

Psychological Impact of Debt

High-interest debt can cause:

- Anxiety

- Sleep issues

- Reduced work performance

- Relationship stress

Financial stability directly affects mental well-being.

Final Thoughts: Borrow Smart, Not Fast

High-interest personal loans are not always bad — but they are risky when:

- Used for non-essential spending

- Taken without repayment planning

- Combined with other debts

Before borrowing, ask yourself these questions:

- Is this a necessity?

- Can I repay comfortably?

- What is the total repayment amount?

- Do I have an emergency fund?

Smart financial planning today prevents a possible debt trap which might come tomorrow.

Call to Action – If you found this article helpful, share it with someone who might be struggling with high-interest personal loans. Financial awareness can save years of stress. Please reach out to us if you’re facing similar situation, so that we can provide appropriate financial counselling and eventually help you with a tailor-made solution based on your needs.